Daily news, project news and industry news

The cost of photovoltaic kilowatt hour has dropped to 0.3 yuan, and the economy has become increasingly prominent, with huge space for technological progress. At present, the proportion of photovoltaic power generation in China is only 4%. It is estimated that the new photovoltaic installed capacity will reach 219GW in 2030, with CAGR=17%. The time for heterojunction battery industrialization is basically ripe, and the planned capacity of the whole industry exceeds 100GW. Investment opportunities: PECVD equipment, new silver paste, and battery/component enterprises with rapid progress.

Core view:

The economy is gradually highlighted, and the development space is broad: photovoltaic technology has a huge space for progress, equipment can be flexibly deployed, and has broad market prospects. In 2021, the photovoltaic LCOE will be reduced to 0.3 yuan/KWh, which has a good economy on both the power generation side and the grid side; The recent strong demand leads to the shortage of silicon materials. With the gradual release of production capacity, the price of silicon materials is expected to fall sharply in 2023; With the continuous progress of technology, the photovoltaic LCOE will be reduced to 0.2 yuan/KWh in 2030. At present, the proportion of photovoltaic power generation in China is only 4%, and there is huge room for development. It is estimated that China's new photovoltaic installed capacity will reach 219GW in 2030, corresponding to CAGR of about 17%.

Heterojunction industrialization accelerates and leads the industry reform: considering the whole life cycle, heterojunction battery is expected to become the solution of LCOE. Its cost structure and process system are quite different from traditional crystalline silicon battery, which will lead the industry reform. At present, the mass production efficiency of heterojunction battery has reached 24.5%, the unit material cost has dropped to 1.15 yuan/W, and the gap with PERC has narrowed to within 10%. The time for industrialization is basically ripe, and the planned capacity of the whole industry has exceeded 100GW. In terms of investment opportunities, we will focus on heterojunction PECVD equipment, new silver paste, and battery/component enterprises with fast layout.

1、 Photovoltaic installation has become market driven, with broad development space

1.1 Economy is gradually highlighted and development space is broad

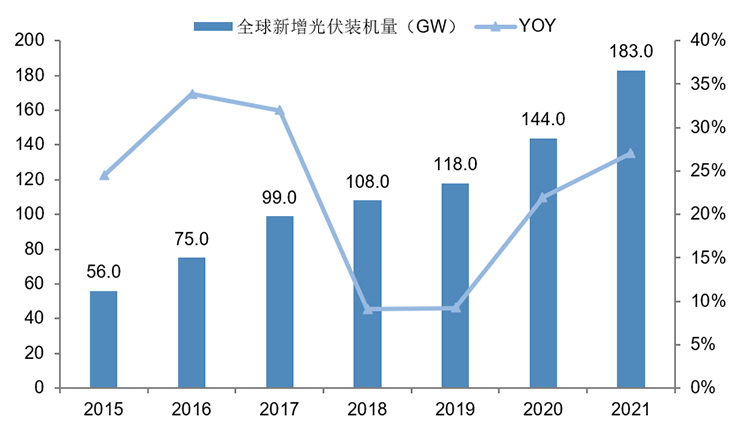

High speed growth of global photovoltaic installation: from 2015 to 2021, the new installed capacity of global photovoltaic increased rapidly from 56GW to 183GW, with CAGR of 22%. On the one hand, Europe and the United States vigorously promote clean energy to replace thermal power. For example, Germany plans to increase the proportion of new energy power generation to 80% by 2030. On the other hand, the conflict between Russia and Ukraine has led to the imbalance of the energy market, a large supply gap of crude oil/natural gas, and sharp price increases; The electricity prices in overseas countries are highly market-oriented, and the end users directly bear the sharp fluctuations of electricity prices, which promotes the strong demand for industrial and commercial/residential self built photovoltaic. It is expected that the global energy structure will accelerate the transformation and promote the rapid growth of photovoltaic installed capacity. CPIA estimates that the new installed capacity of global PV will reach 330GW in 2025, corresponding to a CAGR of 26%.

(Data source: BNEF, capital arrangement of Benyi) Figure 1: New PV installed capacity in the world (2015-2021)

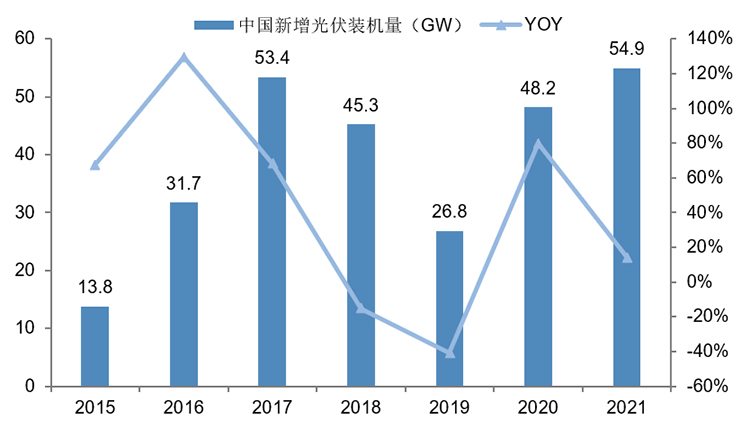

China's PV demand has become market driven: before 2020, due to the policy change and the industry's cost reduction and efficiency increase rhythm are not synchronized, China's PV installed capacity has fluctuated greatly over the years. In the context of the policy subsidy withdrawal and the entry into the era of "affordable Internet access", cost reduction and efficiency increase through technological progress has become the main theme of the industry, and the demand for installed capacity has continued to grow at a high speed. In the first half of 2022, 30.9GW of new installed capacity will be added,+138% year-on-year; PV installations are generally concentrated in the second half of the year, so CIPA expects to increase the installed capacity by 85GW-100GW throughout the year, more than+54.8% year-on-year. We believe that the economy of photovoltaic power generation is gradually highlighted, and the demand will become market driven; At present, the proportion of photovoltaic power generation in China is only 4%, and there is huge development space.

(Source: China Electronics Union, Benyi Capital Arrangement) Figure 2: China's New PV Installed Capacity (2015-2021)

Economy is gradually highlighted: LCOE (Levelled Cost of Energy) is the core index to measure the economy of power generation equipment. With the continuous progress of technology, photovoltaic LCOE has decreased significantly, which is now lower than thermal power. For all participants in the power market, the commercial value of photovoltaic power generation is clear, and it has the basis for large-scale replacement of thermal power from an economic perspective.

(1) Grid side: In 2022, China's wind power/photovoltaic power will be connected to the grid at a parity rate, and the guiding electricity price of each province and city will be 0.24 (Xinjiang) - 0.45 (Guangdong) yuan/KWh; Except Qingdao Overseas, all other administrative regions have dropped below the benchmark price of thermal power, which has a general price advantage. Therefore, for grid operators, the higher the proportion of wind power/photovoltaic power purchased, the higher the profit.

(2) Power generation side: IRENA data shows that since 2010, photovoltaic LCOE has decreased by 88%, onshore wind power LCOE has decreased by 68%, and the annual average is less than 0.3 yuan/KWh in 2022. The cost of wind power/photovoltaic power station is concentrated in the initial investment cost, and there is no need to continuously consume materials during operation; With the progress of technology, the cost of equipment will continue to decline, which will fall below 0.2 yuan/KWh in the long run. On the other hand, thermal power LCOE is about 0.4 yuan/KWh, which fluctuates with the price of fuel (mainly coal); The hydropower LCOE is about 0.3 yuan/KWh. At present, China's hydropower resources are close to the limit of development, and the marginal cost is on the rise.

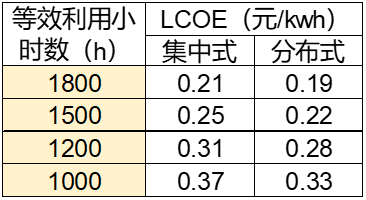

(Source: CPIA, Capital Arrangement of the Home Wing) Table 1: PV kWh Cost (2021)

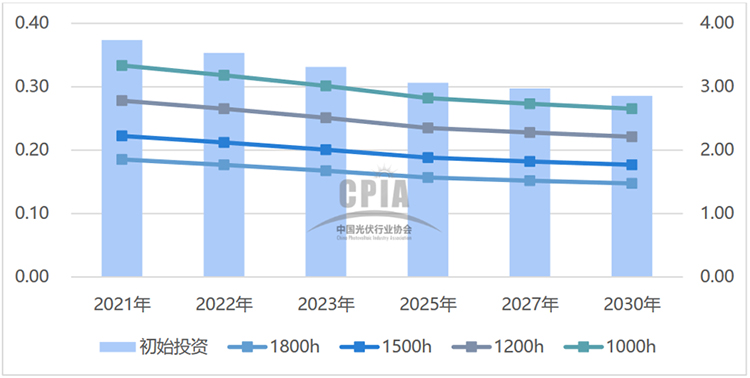

(Data source: CPIA, capital arrangement of this wing) Figure 3: Cost and forecast of distributed photovoltaic kilowatt hour (left axis LCOE, unit: yuan/KWh; right axis initial investment, unit: yuan/W)

(3) Demand side: PV equipment can be modularized and miniaturized for easy deployment, which is suitable for self construction on the demand side. From an economic point of view, if the cost per kilowatt hour of photovoltaic (or photovoltaic+energy storage) is lower than the market price, the data center and other industrial and commercial scenarios can reduce the power cost through self built photovoltaic. In addition, the market price of electricity is widely used by residents in overseas countries, with large fluctuations, so household photovoltaic also has a large development space. BIPV (Building Attached Photovoltaic) refers to the integration of photovoltaic modules and buildings from the design level, so as to reduce the effective power generation area, reduce the heat dissipation demand and reduce the overall cost. The Ministry of Housing and Urban Rural Development and the National Development and Reform Commission proposed to optimize the energy consumption structure of urban construction, and strive to achieve 50% photovoltaic coverage of the roofs of new public institution buildings and new factory buildings by 2025. After the implementation of the standard General Code for Building Energy Conservation and Renewable Energy Utilization in April, many cities across the country have actively issued policies requiring new buildings to install solar energy systems.

(Source: official website of Centrex, capital arrangement of the headquarters) Figure 4: Case: Jiangsu Yizheng Tencent Cloud Data Center adopting BIPV scheme

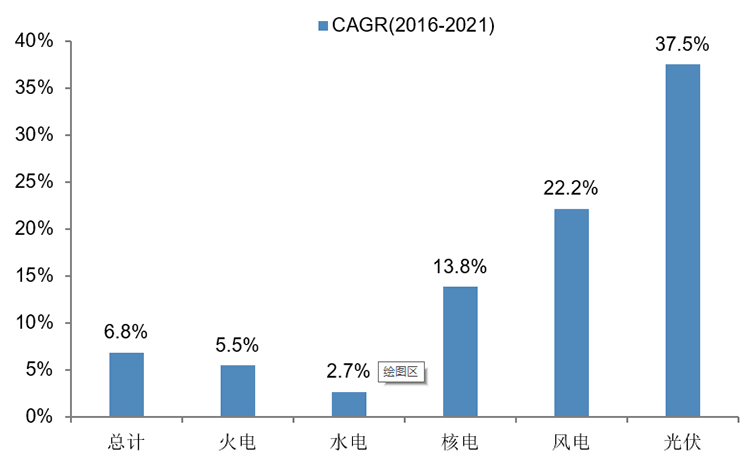

Photovoltaic power generation is still in its infancy, and there is huge room for substitution: in 2021, China's total power generation will be 8.38 trillion kWh,+9.8% year-on-year, and CAGR in the past five years will be 6.8%; PV power generation reached 327 billion kWh,+25.2% YoY, and CAGR reached 37.5% in the past five years. At present, China's photovoltaic power generation accounts for only 4%, which is still in the introduction stage. Taking Germany as an example, the proportion of photovoltaic power generation has exceeded 10% and is expected to reach 30% by 2030. China has formulated a clear carbon neutral development plan, and the PV economy is gradually highlighted. The technology is still making continuous progress. It is expected that China's PV installation will grow at a high speed.

(Source: Energy Administration, Capital Arrangement of the Home Wing) Figure 5: Comparison of Composite Growth of China's Power Generation from Various Sources (2016-2021)

(Source: Energy Administration, capital consolidation of the headquarters) Table 2: Proportion of power generation from various sources in China (2016-2021)

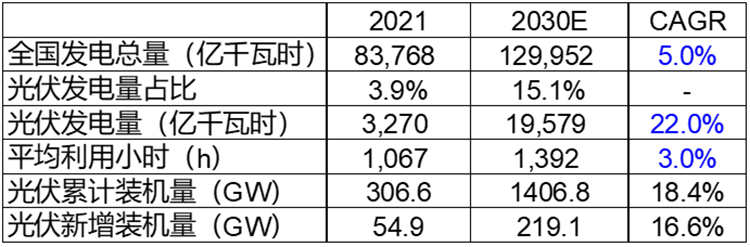

Market space measurement: Assume (1) that the national power generation maintains a compound growth rate of 5%. (2) From 2011 to 2016, the CAGR of wind power generation was 27%, increasing from 1.6% to 4.0%, while from 2016 to 2021, the CAGR was 22%, increasing from 4% to 7.8%. With the increase of the proportion, the composite growth rate decreased slightly. At present, photovoltaic power generation accounts for 3.9%, basically the same as wind power in 2016; The CAGR of photovoltaic power generation in the past five years has reached 37.5%. It is conservatively estimated that the CAGR of 2022-2030 will decrease to 22%, corresponding to 15.1% of photovoltaic power generation in 2030. (3) The actual available hours maintain a compound growth rate of 3%. (4) The service life of photovoltaic equipment is about 20-25 years, so the renewal of stock equipment is not considered temporarily. Based on the above core assumptions, we predict that the new installed capacity in 2030 will be 219GW, and the CAGR will be about 17%.

(Source: Energy Administration, Capital Arrangement of the Headquarters) Table 3: Forecast of China's PV New Installed Capacity in 2030 (the blue part is the core assumption)

Energy storage technology can improve the stability of photovoltaic power generation and enhance competitiveness: due to unstable sunlight, photovoltaic power generation has a large fluctuation, and the energy storage system is equivalent to a "reservoir", which can not only solve the problem of instability of the power system caused by photovoltaic power generation, but also effectively improve the utilization of electricity and the balance between supply and demand, and enhance the competitiveness of photovoltaic. With the gradual withdrawal of thermal power plants and the commercialization of energy storage technology, it is estimated that the new installed capacity of China's photovoltaic will maintain a long-term growth rate of 5-10% from 2030 to 2050.

1.2 In the short term, the price of silicon material runs at a high level, which is expected to fall sharply in 2023

The main line of the PV equipment industry chain is silicon material - silicon chip - battery chip - module. The cost of each link mainly comes from the cost of a single upstream material, and the transmission logic is clear. According to the statistics of CPIA, in 2021, the unit investment cost of China's centralized photovoltaic power plants will be 4.15 yuan/W, of which components will account for about 46% (1.91 yuan/W) and inverters will account for about 5% (0.2 yuan/W). In the short term, the demand for installed capacity is strong and the period of silicon material expansion is long, and the tight supply leads to the price rise of the whole industrial chain; With the release of new capacity, it is expected that the price of silicon material will fall sharply in 2023, ensuring the downstream installed demand and the healthy development of the industry.

The production technology of silicon material is basically mature, and the price depends on the supply and demand relationship: industrial silicon is processed from quartzite and mainly used to produce three types of products: (1) polycrystalline silicon; (2) Organic silicon; (3) Silicon aluminum alloy. According to TBEA, about 1.06 tons of industrial silicon will be consumed to produce 1 ton of polysilicon. Polysilicon is divided into photovoltaic grade polysilicon and electronic grade polysilicon. The purity requirements are different, and the demand ratio is about 9:1. Photovoltaic polysilicon, also known as "silicon material", is the core raw material for preparing photovoltaic silicon chips. At present, the mainstream technology for silicon material production is Siemens method, which is basically mature; In addition, GCL mainly promotes granular silicon technology, which is characterized by low cost and low purity, and runs counter to the demand of photovoltaic cell technology development (N-type batteries put forward higher requirements for silicon material purity), leading to a dull market response. Therefore, the technical attribute of silicon material is weak, while the chemical attribute is strong. The profitability of the enterprise mainly depends on the supply and demand relationship.

The production expansion period is relatively long, and the supply is continuously tight in the near future: silicon is the second abundant element in the crust, accounting for about 26% of the total mass of the crust. In nature, it mainly exists in the form of silicate/silica, which is widely distributed, and theoretically there should be no shortage. However, due to the rigid production capacity of silicon materials, the expansion period is up to 18 months. However, in 2019-20, the silicon material production capacity was seriously excessive. At that time, the industry was pessimistic about the future demand for installed capacity, and did not arrange enough expansion planning. As a result, the silicon material supply has been in a tight balance since 2021, and the price has risen from 80000 yuan/ton to 270000 yuan/ton in November; Since 2022, the price has continued to rise, approaching 300000 yuan/ton.

The intensification of competition will promote the reduction of concentration, and the price is expected to drop significantly in 2023: after multiple rounds of technology iterations and price cycles, the concentration of the polysilicon industry has entered a high range, and Tongwei Shares (Yongxiang Shares), Daquan Energy, Poly GCL, New Special Energy and Dongfang Hope rank among the global echelons. CPIA data shows that in 2021, the global total polysilicon production capacity will reach 774000 tons, and CR10 will be 91.1%; The total output is about 595000 tons, CR5 is 70.6%, and CR 10 is 92.7%. Looking forward to the future, the market prospect of silicon materials will attract a large number of new entrants, such as Hesheng Silicon Industry in the upstream, Shangji CNC, CSI, Runyang, etc. in the downstream. From the perspective of the production expansion progress of enterprises, it is expected that the silicon material capacity will be released on a large scale in 2023, and the price will fall sharply, which will promote the return of the profits of the industrial chain to reasonable distribution, improve the profits of downstream enterprises, and ensure the demand for terminal installation.

1.3 Technology prospect: Heterojunction and TOPCon will become mainstream

Photovoltaic cells directly convert solar energy into electric energy by making use of photovoltaic cells. The trend of technological development is higher photoelectric conversion efficiency, high stability (long life), and controllable cost, which ultimately reflects lower cost per kilowatt hour. Therefore, the decline of cost per kilowatt hour is the standard to measure the advancement of photovoltaic technology. On the one hand, technology is the core driving force of the photovoltaic industry. New technologies drive down the cost of electricity consumption and improve the commercial value of photovoltaic equipment, which is the core factor to promote the growth of photovoltaic installed capacity. On the other hand, technological iteration will also bring about changes in demand for equipment and auxiliary materials in various links, and investment opportunities will emerge.

1.3.2 Crystal silicon battery will remain mainstream

With silicon chip as the core raw material, the crystalline silicon battery has become the mainstream technology route of photovoltaic cells with mature technology, cost and reliability more in line with the needs of commercialization. In the last round of technology iteration cycle, Longji Co., Ltd. adopted the diamond wire cutting process to significantly reduce the cost of monocrystalline silicon batteries and comprehensively replace polycrystalline silicon batteries. At present, monocrystalline silicon PERC batteries occupy the mainstream, accounting for 91.2% of the market in 2021.

It has become an inevitable trend for N-type crystalline silicon battery to replace P-type crystalline silicon battery: according to the type of silicon chip, crystalline silicon battery can be divided into P-type battery and N-type battery. The difference mainly lies in the different impurities diffused during the preparation of silicon chip, which eventually leads to a certain difference in the properties of finished products. At present, the mainstream PERC belongs to P-type battery, TOPCon and heterojunction belong to N-type battery. TOPCon battery and heterojunction battery have significant advantages of high efficiency and low attenuation, and will gradually replace PERC battery in the medium term.

(1) P type battery: only one impurity (boron) needs to be diffused to prepare P type battery, which is low in cost, short in minority carrier life and low in photoelectric conversion efficiency. The process of P-type battery is fully mature, and it occupies the mainstream of the market by virtue of its cost performance advantage. However, the photoelectric conversion efficiency is close to the theoretical upper limit (about 24%).

(2) N-type battery: high efficiency+long life, low electricity cost. N-type battery has long minority carrier life, high photoelectric conversion efficiency, theoretical efficiency can be increased to about 28%, and attenuation rate also has significant advantages. The difficulty lies in the diffusion of two impurities (P+B) when preparing N-type silicon wafers, which is costly. However, after large modulus production, based on the advantages of efficiency and life, the cost per kilowatt hour will be lower than that of P-type batteries. With the gradual maturity of equipment and technology, the cost has dropped significantly. At present, the N-type battery has a strong competitiveness in terms of electricity cost, which will usher in the turning point of commercialization and start the comprehensive replacement of the P-type battery.

Heterojunction and TOPCon will co-exist for a long time and develop in parallel: in the N-type battery system, heterojunction and TOPCon have advantages and disadvantages, and there is no obvious substitution relationship. The mainstream view in the industry believes that the two technology routes will develop in parallel and share the market equally by the 2030's. In the long run, both schemes can be combined with the perovskite technology to develop the laminated battery with higher efficiency.

(1) TOPCon battery: the structure is similar to the traditional crystalline silicon battery, and the process is compatible with the existing production line.

(2) Heterojunction battery: the technical principle/design idea is quite different from the traditional crystalline silicon battery, and a new production line needs to be built. The raw material of heterojunction battery is still mainly silicon chip, which belongs to crystalline silicon battery in a broad sense.

(3) The laminated battery uses perovskite as the auxiliary material to further improve the performance of crystalline silicon battery, which has a broader market prospect in the long run.

1.3.2 Crystal silicon battery will remain mainstream

With silicon chip as the core raw material, the crystalline silicon battery has become the mainstream technology route of photovoltaic cells with mature technology, cost and reliability more in line with the needs of commercialization. In the last round of technology iteration cycle, Longji Co., Ltd. adopted the diamond wire cutting process to significantly reduce the cost of monocrystalline silicon batteries and comprehensively replace polycrystalline silicon batteries. At present, monocrystalline silicon PERC batteries occupy the mainstream, accounting for 91.2% of the market in 2021.

It has become an inevitable trend for N-type crystalline silicon battery to replace P-type crystalline silicon battery: according to the type of silicon chip, crystalline silicon battery can be divided into P-type battery and N-type battery. The difference mainly lies in the different impurities diffused during the preparation of silicon chip, which eventually leads to a certain difference in the properties of finished products. At present, the mainstream PERC belongs to P-type battery, TOPCon and heterojunction belong to N-type battery. TOPCon battery and heterojunction battery have significant advantages of high efficiency and low attenuation, and will gradually replace PERC battery in the medium term.

(1) P type battery: only one impurity (boron) needs to be diffused to prepare P type battery, which is low in cost, short in minority carrier life and low in photoelectric conversion efficiency. The process of P-type battery is fully mature, and it occupies the mainstream of the market by virtue of its cost performance advantage. However, the photoelectric conversion efficiency is close to the theoretical upper limit (about 24%).

(2) N-type battery: high efficiency+long life, low electricity cost. N-type battery has long minority carrier life, high photoelectric conversion efficiency, theoretical efficiency can be increased to about 28%, and attenuation rate also has significant advantages. The difficulty lies in the diffusion of two impurities (P+B) when preparing N-type silicon wafers, which is costly. However, after large modulus production, based on the advantages of efficiency and life, the cost per kilowatt hour will be lower than that of P-type batteries. With the gradual maturity of equipment and technology, the cost has dropped significantly. At present, the N-type battery has a strong competitiveness in terms of electricity cost, which will usher in the turning point of commercialization and start the comprehensive replacement of the P-type battery.

Heterojunction and TOPCon will co-exist for a long time and develop in parallel: in the N-type battery system, heterojunction and TOPCon have advantages and disadvantages, and there is no obvious substitution relationship. The mainstream view in the industry believes that the two technology routes will develop in parallel and share the market equally by the 2030's. In the long run, both schemes can be combined with the perovskite technology to develop the laminated battery with higher efficiency.

(1) TOPCon battery: the structure is similar to the traditional crystalline silicon battery, and the process is compatible with the existing production line.

(2) Heterojunction battery: the technical principle/design idea is quite different from the traditional crystalline silicon battery, and a new production line needs to be built. The raw material of heterojunction battery is still mainly silicon chip, which belongs to crystalline silicon battery in a broad sense.

(3) The laminated battery uses perovskite as the auxiliary material to further improve the performance of crystalline silicon battery, which has a broader market prospect in the long run.

1.3.4 Summary

TOPCon and heterojunction battery in crystalline silicon battery system have reached the turning point of commercialization, and will gradually replace PERC and become the mainstream of the market in the next decade. There are obvious defects in various thin film batteries represented by perovskite, and the commercial feasibility is low. On the other hand, the laminated battery adopts the design idea of combining perovskite and crystalline silicon, which is more promising than the single junction perovskite battery. Therefore, in the absence of breakthrough progress in new materials, it is expected that the crystalline silicon battery will remain the mainstream.

2、Investment opportunity analysis: focus on heterojunction industrialization

The development prospect of heterojunction battery is clear, the cost is close to PERC, and the demand for expansion of enterprises is strong, which will soon enter the stage of large-scale industrialization. Due to the great difference between the process system and the demand for materials and the traditional crystalline silicon battery, the commercialization of heterojunction battery will bring about a reshuffle of the industrial pattern and a large number of investment opportunities.

2.1 Heterojunction has significant performance advantages and clear cost reduction path

2.1.1 Symmetrical structure is adopted, with significant performance advantages

Heterojunction battery is called Intrinsic Thin layer (HJT) in full. It adopts symmetrical structure. On both sides of N-type silicon wafer are intrinsic amorphous silicon film (amorphous I layer), PN junction (amorphous N layer and amorphous P layer), TCO transparent conductive film, and silver electrode. The innovative structure design enables the heterojunction battery to have four advantages: high efficiency, low attenuation, high temperature resistance and high double-sided ratio.

(1) High efficiency: The core advantage of the heterojunction battery is the excellent passivation effect of the intrinsic amorphous silicon film (the red "amorphous I layer" in the figure above). The efficiency of photovoltaic cells is mainly determined by the minority carrier lifetime excited by light. Under the traditional crystalline silicon cell structure, minority carriers are easily captured and recombined by the dangling bonds on the silicon surface, which leads to the reduction of cell efficiency. Deposition of hydrogen rich intrinsic amorphous silicon films on both sides of silicon wafer by heterojunction batteries can effectively hydrogenate the dangling bonds and reduce surface defects, thereby significantly improving minority carrier life, increasing open circuit voltage and improving battery efficiency. The theoretical efficiency of heterojunction battery can reach 28.5%, and the current laboratory efficiency is 26.5%; The efficiency of mass production components has reached 24.5%, which has an advantage of 1.2% over PERC.

(2) Low attenuation and long service life: TCO film of heterojunction battery has conductive characteristics, and the charge will not produce polarization on the surface, and will not produce potential induced attenuation (PID), which is superior to PERC and TOPCon; N-type silicon wafer is phosphorus doped, without boron oxygen complex and boron iron complex, so the light induced attenuation (LID) is consistent with TOPCon and far superior to PERC.

(3) High temperature resistance (low temperature coefficient): The initial nominal power of photovoltaic modules is the data in the environment of 25 ℃ (STC standard conditions), but in actual operation, the working temperature is about 50 ℃ for most of the time. The heterojunction battery is extremely stable at high temperature, and can still maintain a relative efficiency of more than 90% at 60 ℃, which is far superior to PERC and TOPCon batteries.

(4) High double-sided ratio: the three-layer film on the front and back of the heterojunction battery and TCO are transparent and symmetrical in structure. It is naturally a double-sided battery, and the double-sided ratio can reach 90% - 98%. For comparison, PERC and TOPCon can only achieve 80%-85% double-sided ratio.

Summary: On the one hand, the performance of heterojunction battery is far better than that of PERC; On the other hand, although the nominal conversion efficiency is the same as TOPCon, the heterojunction battery has the advantages of low attenuation+high temperature resistance+high double-sided ratio, and the actual conversion efficiency is higher than TOPCon. Therefore, considering the whole life cycle, the cost per kilowatt hour of heterojunction battery will be lower than that of other technology routes.

2.1.2 The cost reduction path is clear, and it is close to commercialization

Clear cost reduction path: Heterojunction technology requires the cooperation of all links of the whole industry chain to explore and optimize cost reduction schemes on the premise of ensuring performance. Four major cost reduction paths: equipment, silver coated copper paste, ultra-thin silicon wafer, and microcrystalline technology.

(1) Since 2019, with the promotion of equipment manufacturers such as Maiwei, heterostructure equipment has been fully localized, and the unit investment has dropped from 1 billion to 350 million/GW; As more battery/component projects begin to advance, mature plans will be formed for equipment and large-scale production will be realized. It is estimated that the unit investment will drop below 300 million/GW in 2024.

(2) The cost reduction of silver paste is divided into five steps: multiple main grids, steel plate printing, silver clad copper, SWCT and copper plating. At present, the consumption of positive silver is mainly reduced by multi main grid technology and reducing grid line width, while steel plate printing and silver coated copper have also made some progress. According to the statistics of CPIA, the consumption of double-sided low-temperature silver paste of heterojunction battery will be about 190mg/piece in 2021, a year-on-year decrease of 14.9%, and it is expected to drop to 100mg/piece in 2030.

(3) Ultra thin silicon chip+microcrystalline technology improves efficiency and consumes less silicon per watt. 166mm+165 μ The silicon consumption per watt of m PERC module is 1.4g, TOPCon is 1.3g+, and the heterojunction can be reduced to 130 μ M thick, the average silicon consumption of 500W module is only 0.513g per watt. The microcrystalline technology refers to coating a layer of crystalline silicon film on the amorphous silicon film to further improve efficiency. This scheme has entered the production line of Huasheng and other enterprises for mass production verification.

The conditions for commercialization are basically mature, and the demand for expansion is strong: based on the comprehensive public information, the gap between the cost of single watt materials of heterojunction batteries and that of PERC batteries is currently within 10%, and it is expected to fall below the cost of PERC in 2023. The good economy urges battery/module manufacturers to accelerate the planning of heterostructure expansion. By the end of 2021, the domestic heterostructure production capacity will reach 5.57GW, dominated by pilot lines. According to statistics, the new capacity of heterojunction in the whole industry has exceeded 109GW. It is estimated that 20-25GW will be added in 2022 and 40-50GW will be added in 2023. As of June 2022, there are 4 companies with actual capacity of more than 1GW: Huasheng New Energy, Aikang Technology, Tongwei Shares and Jinggang Glass. The entrants can be divided into three categories: new forces, reformers (traditional enterprises) and dilemma turnover.

2.2 Equipment: focus on PECVD

A new production line is needed for heterojunction batteries: the production process of heterojunction batteries includes four processes: cleaning and velvet making, amorphous silicon film deposition, TCO preparation, and silk screen curing. Amorphous silicon film deposition and TCO preparation are new processes, which require the use of advanced new equipment. The other two processes also have stricter requirements on cleanliness, fineness, uniformity and continuity. Therefore, the heterojunction battery production line is incompatible with the traditional crystalline silicon battery production line, and new production lines must be built.

The downstream construction and production demand is strong, and the equipment manufacturers welcome development opportunities: at present, a single GW heterojunction battery production line requires an investment of 350 million yuan to 450 million yuan. According to statistics, at present, the new capacity planning of heterostructure in the whole industry has exceeded 109GW. Jinchen Group estimates that there will be about 25GW of new project equipment orders for heterojunction equipment in the whole industry in 2022, and 40-50GW of new project equipment orders in 2023. Assume that the investment amount of a single GW in 2022 and 2023 is RMB 400 million/350 million respectively, and the corresponding market scale of heterostructure equipment is RMB 10 billion/17.5 billion respectively.

Focus on the core equipment PECVD: PECVD (Plasma Enhanced Chemical Vapor Deposition) is required for the preparation of amorphous silicon films for heterojunction batteries. Glow discharge plasma is used to decompose silane and other gas source molecules, so as to realize the preparation of amorphous silicon films. Its performance directly affects the battery efficiency. Because the functional requirements of each layer of amorphous silicon film are different, the requirements for the preparation process are different, and they need to be completed in multiple chambers. Therefore, the multi chamber deposition system needs to be introduced into the heterojunction PECVD equipment, which puts forward higher requirements for the overall design of the equipment and the multi chamber process control. On the other hand, PECVD accounts for 50% of the investment cost of heterostructure production line equipment. Based on the calculation of the cost of a single GW of RMB 200 million/175 million in 2022/2023, the corresponding market size is RMB 5 billion/8 billion in 2022/2023.

The industry threshold is high and the player advantage is obvious: at present, domestic equipment is widely used in domestic heterojunction production lines, and there are five companies with the ability to deliver heterojunction PECVD equipment: Maiwei, Jiejia Weichuang, Junshi Energy (unlisted), Ideal Wanlihui (unlisted) and Jinchen. The first four of them will begin to lay out heterojunction PECVD equipment at least before 2019.

Maiwei Shares can provide whole line equipment and its market share: as the leader of screen printing equipment, Maiwei Shares makes a comprehensive layout in the field of heterojunction equipment, has the ability to deliver whole line equipment, and is developing towards the overall solution provider of heterojunction battery production line. Its market position will rise. From the current construction bidding situation, Maiwei is the largest company with a market share of more than 70%. Huasheng, Jingang Glass, Aikang, Mingyang, Reliance Industry and other projects all adopt Maiwei as the whole line plan. Assume that the market share of Maiwei will be 70%/60% respectively in 2022/2023, and the corresponding order amount of heterojunction equipment will be RMB 7/10.5 billion, far exceeding the company's total revenue in 2021 (RMB 3.095 billion).

Jinchen has entered the customer verification stage: in 2021, the company's PECVD equipment has been introduced into Jinneng Science and Technology's heterojunction pilot line. The process flow will start in August, and the average efficiency of the battery chip will reach 24.38% in December. In the process of assembly and test, PECVD equipment based on microcrystalline has been in deep contact with customers. It is expected that the first one will be delivered to customers in the second half of the year for verification at the pilot scale/mass production level (it is rumored that the customer is Longji Green Energy). Assuming that the market share of Jinchen PECVD will reach 10% in 2023, it will bring an order volume of 800 million yuan, which is about 50% of the company's total revenue in 2021.

2.3 Auxiliary materials: both quantity and price of new silver paste rise

Silver paste is printed on both sides of the photovoltaic cell as an electrode material, which is mainly used to derive the electrical energy generated by the cell. Its performance directly affects the efficiency of the photovoltaic cell. Silver is a highly conductive metal material with high cost, but it brings greater gain to the cell efficiency and lower cost per kilowatt hour. Therefore, it has become a solution for photovoltaic cell electrode materials.

2.3.1 Clear market prospect

The demand for silver paste of heterojunction battery doubled: silver paste is an important auxiliary material of photovoltaic cell chip, and its cost proportion is only second to silicon chip. At present, the unit silver paste demand of P-type/TOPCon/heterojunction battery is 96.4/145.1/190.0 mg respectively; Silver paste accounts for about 8% of the cost of P-type battery and 25% of the cost of heterojunction battery, and the demand is greatly increased. With the industrialization of TOPCon and heterojunction, the market share will increase, and the growth rate of silver paste demand will exceed the growth rate of photovoltaic installation.

The market size will exceed 50 billion yuan: according to the statistics of Asiachem Consulting, the global total demand for silver paste will reach 4000 tons in 2022; According to the average price of 5300 yuan/kg, the market scale is about 21.2 billion yuan. CPIA believes that the demand for silver paste per unit of heterojunction battery will remain at the level of 100mg in 2030, even considering the decrease in demand for silver paste per unit caused by technological progress. It is estimated that the market size of silver paste will maintain a long-term compound growth rate of 17% (consistent with the growth rate of photovoltaic installed units), and the market size will exceed 50 billion yuan in 2030.

2.3.2 Profitability recovery

Since 2015, domestic silver paste enterprises have developed rapidly, and Dike, Jingyin New Material (Suzhou Gutechnetium), Juhe and other enterprises have accelerated their production expansion to seize market share. The domestic rate of silver paste has increased from 5% to 70%, and CR3 has increased from 35% in 2019 to 55% in 2021. Over the same period, the gross profit rate decreased significantly, from 18% in 2019 to 10% in 2021. On the one hand, at this stage, there is a huge room for domestic substitution, attracting a large number of enterprises to enter, and the price competition is fierce; On the other hand, the high price of silicon material has led to the pressure on the profits of downstream battery manufacturers. As an important non silicon auxiliary material of battery chips, silver paste has limited bargaining space. Looking into the future, the heterojunction silver paste has higher technical requirements, and it is expected that the gross profit margin of the technical silver paste enterprises will rise again.

Low temperature silver paste has stronger premium ability: there are two types of silver paste: high temperature silver paste and low temperature silver paste. P type battery and TOPCon battery use high temperature silver paste, and the sintering temperature is above 500 ℃; The amorphous silicon film of heterojunction battery is more sensitive to temperature, so the manufacturing temperature should be controlled below 250 ℃, and low-temperature silver paste should be used. Low temperature silver paste is different from high temperature silver paste in terms of process, curing temperature, curing time, etc. It is also necessary to make targeted adjustments to the resistivity, welding adhesion, chemical stability and other properties according to the specific requirements of heterojunction batteries, so that the technical difficulty is improved and the premium ability is stronger. In 2021, the price of high-temperature silver paste will be about 5000-5500 yuan/kg, while the price of low-temperature silver paste will be about 6500 yuan/kg. With basically the same cost, the price difference will be more than 1000 yuan/kg. At present, the low-temperature silver paste market is mainly controlled by Kyoto Electronics of Japan, and the market share will exceed 90% in 2021. The strategic plan of Kyoto Electronics is conservative, and the expansion plan has not been formulated yet. Therefore, as the demand for heterojunction batteries increases, the market share of Chinese enterprises with technology will increase rapidly.

Silver coated copper technology reduces material cost and improves technical threshold: silver powder is the core raw material of silver paste, accounting for about 95% of the cost. In order to reduce the material cost, the enterprise proposed the silver clad copper technology. The copper powder was placed in the silver nitrate solution to prepare the "silver clad copper powder" of outer layer silver+inner layer copper. The cost of copper is far lower than that of silver, and the cost of silver nitrate is also lower than that of silver powder. Therefore, using silver coated copper powder to replace pure silver powder to prepare silver paste can greatly reduce the material cost while ensuring the conductivity. At present, silver clad copper technology is widely concerned by downstream customers and is expected to become the mainstream, but no mature scheme has been formed. Enterprises that take the lead in achieving breakthroughs are expected to stand out in the heterojunction era and become industry leaders.

2.3.3 Investment opportunities: focus on cutting-edge technology and upstream integration

The technical threshold of low-temperature silver paste and silver clad copper is relatively high. The leading enterprises such as Dike, Juhe and Jingyin New Materials have made rapid progress and will enjoy the dividends brought by the industrialization of heterojunction batteries. In addition, Dike adopts the vertical integration strategy to promote the upstream silver powder layout and improve the technical barriers.

Dike adopts a vertical integration strategy to continuously expand its upstream layout. The planned capacity of silver nitrate is 5000 tons, and 1000 tons will be put into production in 2023Q1. The planned capacity of silver powder+silver coated copper powder is 2000 tons, which is planned to be put into production in 2024; Silver powder has been distributed earlier and has obtained invention patents. Silver coated copper powder has also experienced a 2-year technical reserve period. Low temperature silver paste products have entered the supply chain of Huasheng and Tongwei. In addition, Dike is promoting the acquisition of DuPont's silver paste business. If the acquisition is successful, it will obtain 15 heterojunction low-temperature silver paste patents, accelerating the improvement of the company's product strength.

The sales volume of low-temperature silver paste of new crystal silver material in 2021 will be 5.14 tons; The silver clad copper scheme aims to reduce the cost by more than 30%. At present, the main grid has passed the reliability test and has been verified by the outdoor demonstration power station at the client. 50% silver containing fine grids have entered small batch mass production. Juhe Shares (to be listed) has also completed the development of heterojunction low-temperature silver paste products, and can reach the same level of imported products in terms of printability, volume resistivity and welding tension.

2.4.1 New forces

At present, there is a strong demand for photovoltaic installation, while the heterojunction battery uses a new process system, which is quite different from the traditional crystalline silicon battery. The new entrants ushered in the strategic window period of entry competition, represented by Huasheng New Energy (unlisted).

Strong team strength: In July 2020, Huasheng New Energy was established in Xuancheng, Anhui Province, focusing on the R&D and industrialization of heterojunction batteries. By the end of 2021, a round A financing of 800 million yuan will be completed, and Hefei Industrial Investment Corporation, China Merchants Bank International and other shareholders will be introduced. The company's core personnel have rich technical reserves and industrial experience. Chairman Xu Xiaohua was once the vice president of Hanergy Thin Film Power (00566. HK, delisted); CTO Wang Wenjing was once the director of the Solar Cell Technology Research Office of the Institute of Electrical Engineering, Chinese Academy of Sciences; CEO Zhou Dan was the chairman and general manager of Tongwei Solar.

Actively expand capacity and product efficiency in the industry: by June 2022, Xuancheng Phase II will be put into production, and the company's capacity of heterojunction batteries and modules has reached 2.7GW; The total capacity will exceed 10GW by the end of 2023. Xuancheng Phase II adopts single-sided microcrystalline technology. At present, the average conversion efficiency of mass production has reached 24.5%, reaching the industry level, and is expected to increase to 25-25.2% within the year; In 2023, double-sided microcrystalline technology will be introduced to impact the conversion efficiency of more than 25.5%. The company aims to ship 4-5GW of heterojunction components in 2023 (corresponding revenue of about 10 billion yuan). From the Shuangliang Energy Conservation Announcement, Huasheng has signed a purchase agreement to purchase 7800 tons of single crystal ingots from 2022 to 2025, which is estimated to meet the production demand of 3.4GW batteries. It is expected that Huasheng is expected to seize the strategic window period of heterojunction and become the forefront of the industry.

2.4.2 Reformers (traditional enterprises)

Among traditional battery/component enterprises, Tongwei and Dongfang Risheng are actively promoting the industrialization of heterojunction. It is estimated that more than 15GW of capacity will be put into operation in 2023. Longji Lvneng has no large-scale construction and production plan for the time being, but the R&D progress has been maintained and the heterojunction efficiency record has been broken many times.

Tongwei Shares: start trial production of heterojunction batteries at the end of 2018; In July 2021, the world's first 1GW pilot line will be put into production, and the equipment schemes of many enterprises will be used for comparative testing, laying a good foundation for large-scale construction and production; This project is regarded as the "training ground" of heterojunction equipment manufacturers, and is widely concerned by the industry. In April 2022, it will be announced to build a 32GW annual output "high efficiency crystalline silicon project", with a planned investment of 6 billion yuan in Phase 1, and a 16GW capacity will be built by the end of 2023. The unit investment of the project is 375 million yuan/GW, which matches the investment demand of the heterostructure production line. Therefore, there is a view in the industry that the project is a heterostructure production line.

Dongfang Risheng: The 500MW heterojunction pilot line of Jintan Factory has been put into operation, and it is expected to achieve GW shipment in 2023Q1. Ningbo 15GW heterojunction battery chips and modules will be constructed in two phases, with a total development and construction period of 30 months, and are expected to be put into production in 2023-2024. The company's Fuxi series heterojunction module adopts 120 μ The 210 half cut silicon chip, microcrystalline technology and 24BB technology with thickness of m and four corners chamfer have a power of up to 700W+, battery efficiency of 25.5% and module efficiency of 22.53%; LCOE decreased by nearly 10% compared with PERC components.

Longji Lvneng: technology, construction and production planning are not determined. In terms of technology research and development, two lines are parallel, which has refreshed the efficiency records of TOPCon and heterojunction batteries for many times. However, they are cautious about capacity construction, and are still evaluating the development prospects of TOPCon and heterojunction. Li Zhenguo of Longji believes that the investment in photovoltaic cell production line is very large. If the technical route is judged wrong, the enterprise is likely to lose competitiveness, so Longji temporarily chooses to wait and see. In 2022, Longji announced the construction of 1.2GW heterostructure pilot line. Some people believed that the project was similar to the Jintang pilot line of Tongwei in 2021. Before large-scale construction, it demonstrated and compared the performance of equipment of various manufacturers, which was consistent with the information disclosed by Jinchen. If the pilot scale test progresses smoothly, Longji is expected to start large-scale construction of heterostructure capacity in 2023.

2.4.3 Dilemma reversal

Heterojunction batteries bring disruptive development opportunities, while some listed companies' main businesses are stuck in a bottleneck. They hope to change their development prospects by entering the field of heterojunction batteries. On behalf of the company, they are Aikang Technology and Jinggang Glass. The two enterprises laid out the heterojunction technology early, and the early investment was large, which led to losses in recent years. From the public information, the heterojunction technology and construction planning of the two enterprises are progressing smoothly, with a high degree of concern in the industry, which has been recognized to some extent and deserves attention. If the heterojunction capacity is successfully commercialized and the product capacity reaches the first-line level, the fundamental logic will face a reversal.

Reliable and efficient from SENTA

Follow us